Production Possibilities Curve (PPC):

- A graphical representation showing the maximum combinations of goods or services that can be produced with available resources and technology.

Opportunity Cost:

- The value of the next best alternative that is forgone when making a choice, illustrated by the slope of the PPC.

Scarcity:

- The fundamental economic problem where resources are limited while human wants are unlimited, depicted by the PPC boundary.

Choice:

- The decision-making process in selecting which goods and services to produce within the limits of the PPC.

Unemployment:

- When resources, especially labor, are not fully utilized, shown as a point inside the PPC.

Efficiency:

- Maximizing output from available resources, represented by any point on the PPC curve.

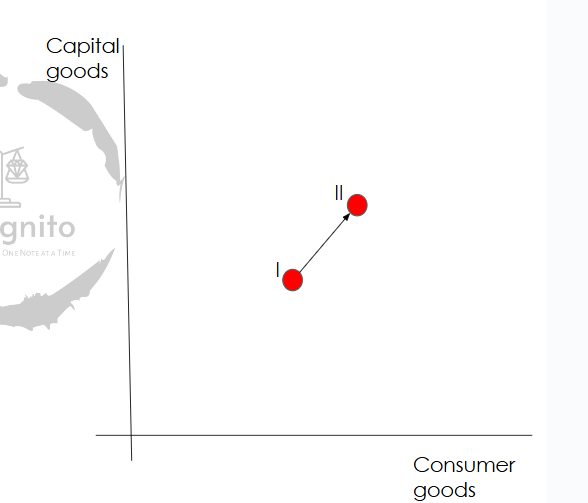

Actual Growth:

Credit to: savemyexams

- An increase in output shown by a movement from a point inside the PPC to a point on the curve, indicating better utilization of resources.

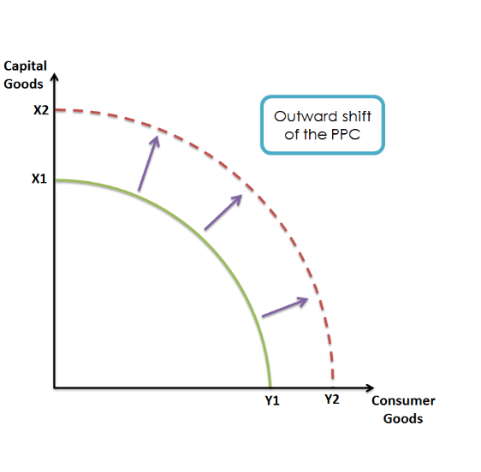

Growth in Production Possibilities:

Credit to: savemyexams

- An outward shift of the PPC, indicating an increase in an economy’s capacity to produce goods and services due to factors like improved technology or increased resources.

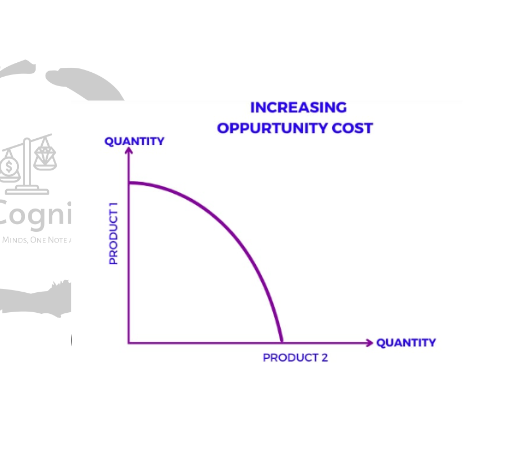

Increasing Opportunity Cost:

Credit to: savemyexams

- As more of one good is produced, the opportunity cost increases,

- shown by the bowed-out shape of the PPC.

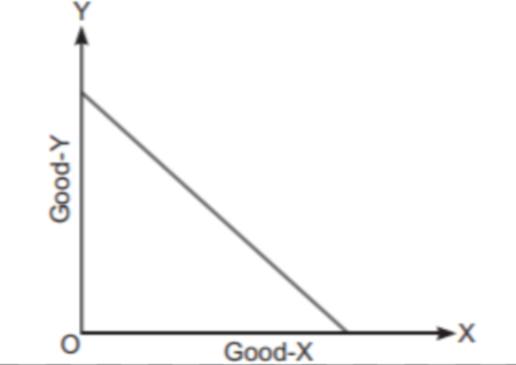

Constant Opportunity Cost:

Credit to: savemyexams

- A straight-line PPC indicating that the opportunity cost of producing one good in terms of another remains constant.

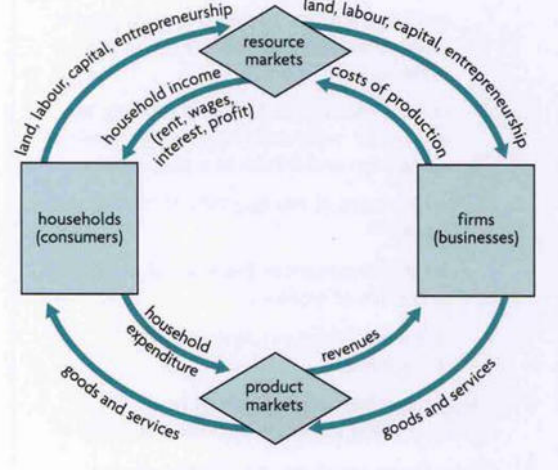

Circular Flow of Income Model:

Credit to: savemyexams

- A model illustrating the flow of goods and services, resources, and money in an economy between households and firms.

- It shows how economic activity is interrelated.

Households and Firms

Households

- Consumers who provide factors of production (land, labor, capital, and entrepreneurship) to firms and receive income (wages, rent, interest, and profits) in return.

Firms

- Businesses that produce goods and services, which they sell to households and other firms.

- They pay households for the use of factors of production.

Goods and Services Market:

- Where households purchase goods and services produced by firms.

- This represents consumer spending in the economy.

Factor Market:

- Where firms hire factors of production from households. This includes the labor market, capital market, and land market.

Injection:

- Additions to the economy that increase the flow of income. They include investment (I), government spending (G), and exports (X).

- Investment (I): Spending by firms on capital goods like machinery and buildings that will be used for future production.

- Government Spending (G): Expenditures by the government on goods and services, such as infrastructure, education, and healthcare.

- Exports (X): Goods and services produced domestically and sold to foreign buyers, bringing money into the domestic economy.

Leakages:

- Withdrawals from the economy that reduce the flow of income. They include savings (S), taxes (T), and imports (M).

- Savings (S): Income not spent by households on goods and services, instead deposited in financial institutions.

- Taxes (T): Payments made by households and firms to the government, which are not available for spending on goods and services.

- Imports (M): Goods and services purchased from foreign countries, leading to money flowing out of the domestic economy.

Equilibrium in the Circular Flow

- Occurs when the total injections (I + G + X) equal the total leakages (S + T + M), leading to a stable flow of income in the economy. If injections exceed leakages, the economy grows; if leakages exceed injections, the economy contracts.